Navigating Nasdaq’s Correction and Market Uncertainty: Preparing for What Lies Ahead

The Nasdaq has entered correction territory, having fallen more than 10% from its recent peaks. Meanwhile, the other two major U.S. stock indexes—the S&P 500 and the Dow Jones Industrial Average—have dropped 8% and 7% over the past month, respectively. This recent wave of stock selling has sparked worries about a potential 2025 bear market and recession. The CNN Fear and Greed Index, which gauges the emotional drivers behind market movements, currently sits in the “extreme fear” zone.

For investors, this is a period of high uncertainty. The S&P 500 Volatility Index—another key indicator of market unease—has climbed to levels last seen in 2022, when high inflation and concerns over rising interest rates roiled markets. Before that, the index reached similar heights during the pandemic, amid uncertainty around COVID-19 outbreaks. I bring up these events because they share a common thread with every market dip: this time feels different.

Is This Time Actually Different?

I recall the stock market turmoil during the pandemic. I usually avoid the word “crash” because it often comes off as hyperbole, but the spring of 2020 was undoubtedly a crash. Stocks plummeted so rapidly that trading was halted multiple times. One of the longest Wikipedia articles I’ve ever read—nearly 10,000 words long with over 500 sources—is titled simply “2020 stock market crash.” Back then, I felt intense uncertainty about the market’s future. Even though I knew the market had weathered similar (and far worse) declines before, there was always that lingering question: Is this time different?

Right now, it’s unclear whether the current bull market will shift to a bear market or if a 2025 recession will materialize—both outcomes could easily be avoided. This dip might end up being a minor blip, one we’ll barely remember a year from now. Or it could mark the start of a larger selloff; there’s no way to know for sure. But if history tells us anything about the future, it’s that this time won’t be different. Like all market corrections, it may feel and look unique, but the stock market always recovers—and usually much faster than expected.

How to Prepare for a Potential Bear Market

I don’t want to claim you should never adjust your investment portfolio in response to market declines, because that’s not true. The recent selloff might make you realize you’ve taken on more risk than you should, and that you need to scale back. However, any portfolio changes should be based on data and evidence—not emotions. The market may feel terrifying right now, but will a 2025 bear market seriously derail your retirement plan? If you’re retired and have 100% of your money in the S&P 500, the answer is likely yes, and you’d probably need to adjust your investments. But if your portfolio has a risk-appropriate mix of stocks and bonds, the answer is almost certainly no.

Personally, I’ve never met anyone who wishes they’d sold all their investments and moved to cash right before a sharp market drop. You rarely hear phrases like, “We wish we’d sold everything in 2008” or “I can’t believe we didn’t cash out right before the pandemic.” What I do hear are regrets about making hasty portfolio changes. The fear and emotion of a market decline can trigger impulsive reactions—sometimes big, costly changes that people later regret.

Don’t just take my word for it, though. Let’s look at the data on what happens after a bear market.

The Data: What Happens Post-Bear Market

When it feels like the worst possible time to be invested in stocks, it’s often the best time to be an investor. I know that sounds contradictory, but it’s true: the market frequently delivers some of its strongest returns when optimism is at its lowest. Is there a more hopeless moment than hitting the absolute bottom of a bear market? Think back to March 2020, in the thick of the pandemic, or March 2009, during the housing crisis—those were the bottoms, and they felt bleak.

Here’s how the market performs once it hits that low point: the average one-month return after a bear market bottom is nearly 15%! One year after reaching the bottom, the S&P 500 is up an average of 43.51%. Stock market recoveries tend to happen very quickly once the bottom is in—and that’s why making sudden changes to your investment strategy can be harmful.

The S&P 500 also delivers strong returns after entering bear market territory, not just after hitting the bottom. The chart below shows the index’s average returns from the day it officially enters a bear market. In many cases, the S&P 500 still has room to fall before bouncing back. Even so, the average returns remain impressive: on average, you can expect the S&P 500 to gain 14% in the year following a bear market entry. For long-term investors, the outlook is even better: over the 10 years after entering a bear market, the index climbs an average of 122%.

Final Thoughts

Dealing with stock market volatility is never enjoyable. For most people, retirement savings are tied, at least in part, to market performance—and the thought of that savings being at risk is terrifying. While every event that triggers a bear market looks distinct, recoveries often follow a similar pattern: they’re quick, and the market’s performance after hitting bottom (and after entering a bear market) is exceptional.

Making major portfolio changes driven solely by emotion and fear is rarely a good idea. But it is always worth checking if the level of risk in your portfolio aligns with your ability to handle risk and your long-term retirement goals.

Home

detail

How To Prepare for a Bear Market in 2025

2025-09-16T18:10:14

Navigating Nasdaq’s Correction and Market Uncertainty: Preparing for What Lies Ahead

The Nasdaq has entered correction territory, having fallen more than 10% from its recent peaks. Meanwhile, the other two major U.S. stock indexes—the S&P 500 and the Dow Jones Industrial Average—have dropped 8% and 7% over the past month, respectively. This recent wave of stock selling has sparked worries about a potential 2025 bear market and recession. The CNN Fear and Greed Index, which gauges the emotional drivers behind market movements, currently sits in the “extreme fear” zone.

For investors, this is a period of high uncertainty. The S&P 500 Volatility Index—another key indicator of market unease—has climbed to levels last seen in 2022, when high inflation and concerns over rising interest rates roiled markets. Before that, the index reached similar heights during the pandemic, amid uncertainty around COVID-19 outbreaks. I bring up these events because they share a common thread with every market dip: this time feels different.

Is This Time Actually Different?

I recall the stock market turmoil during the pandemic. I usually avoid the word “crash” because it often comes off as hyperbole, but the spring of 2020 was undoubtedly a crash. Stocks plummeted so rapidly that trading was halted multiple times. One of the longest Wikipedia articles I’ve ever read—nearly 10,000 words long with over 500 sources—is titled simply “2020 stock market crash.” Back then, I felt intense uncertainty about the market’s future. Even though I knew the market had weathered similar (and far worse) declines before, there was always that lingering question: Is this time different?

Right now, it’s unclear whether the current bull market will shift to a bear market or if a 2025 recession will materialize—both outcomes could easily be avoided. This dip might end up being a minor blip, one we’ll barely remember a year from now. Or it could mark the start of a larger selloff; there’s no way to know for sure. But if history tells us anything about the future, it’s that this time won’t be different. Like all market corrections, it may feel and look unique, but the stock market always recovers—and usually much faster than expected.

How to Prepare for a Potential Bear Market

I don’t want to claim you should never adjust your investment portfolio in response to market declines, because that’s not true. The recent selloff might make you realize you’ve taken on more risk than you should, and that you need to scale back. However, any portfolio changes should be based on data and evidence—not emotions. The market may feel terrifying right now, but will a 2025 bear market seriously derail your retirement plan? If you’re retired and have 100% of your money in the S&P 500, the answer is likely yes, and you’d probably need to adjust your investments. But if your portfolio has a risk-appropriate mix of stocks and bonds, the answer is almost certainly no.

Personally, I’ve never met anyone who wishes they’d sold all their investments and moved to cash right before a sharp market drop. You rarely hear phrases like, “We wish we’d sold everything in 2008” or “I can’t believe we didn’t cash out right before the pandemic.” What I do hear are regrets about making hasty portfolio changes. The fear and emotion of a market decline can trigger impulsive reactions—sometimes big, costly changes that people later regret.

Don’t just take my word for it, though. Let’s look at the data on what happens after a bear market.

The Data: What Happens Post-Bear Market

When it feels like the worst possible time to be invested in stocks, it’s often the best time to be an investor. I know that sounds contradictory, but it’s true: the market frequently delivers some of its strongest returns when optimism is at its lowest. Is there a more hopeless moment than hitting the absolute bottom of a bear market? Think back to March 2020, in the thick of the pandemic, or March 2009, during the housing crisis—those were the bottoms, and they felt bleak.

Here’s how the market performs once it hits that low point: the average one-month return after a bear market bottom is nearly 15%! One year after reaching the bottom, the S&P 500 is up an average of 43.51%. Stock market recoveries tend to happen very quickly once the bottom is in—and that’s why making sudden changes to your investment strategy can be harmful.

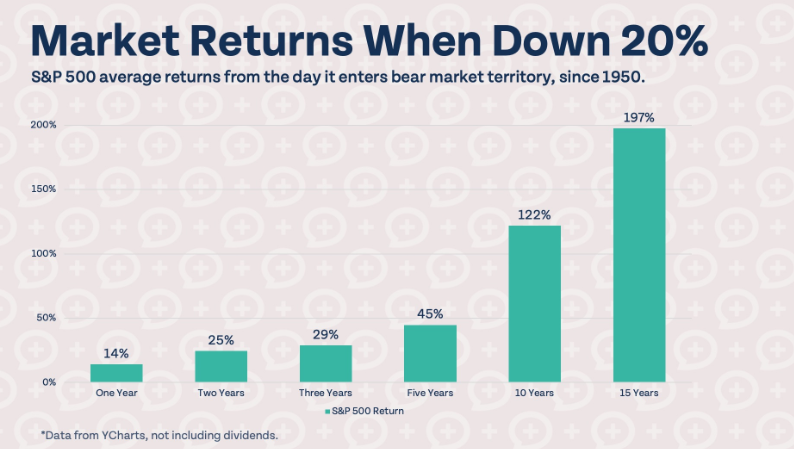

The S&P 500 also delivers strong returns after entering bear market territory, not just after hitting the bottom. The chart below shows the index’s average returns from the day it officially enters a bear market. In many cases, the S&P 500 still has room to fall before bouncing back. Even so, the average returns remain impressive: on average, you can expect the S&P 500 to gain 14% in the year following a bear market entry. For long-term investors, the outlook is even better: over the 10 years after entering a bear market, the index climbs an average of 122%.

Final Thoughts

Dealing with stock market volatility is never enjoyable. For most people, retirement savings are tied, at least in part, to market performance—and the thought of that savings being at risk is terrifying. While every event that triggers a bear market looks distinct, recoveries often follow a similar pattern: they’re quick, and the market’s performance after hitting bottom (and after entering a bear market) is exceptional.

Making major portfolio changes driven solely by emotion and fear is rarely a good idea. But it is always worth checking if the level of risk in your portfolio aligns with your ability to handle risk and your long-term retirement goals.