Some financial influencers argue that credit cards should never be used, while others view them as a useful tool in managing personal finances. Are credit cards harmful, or are they beneficial? The reality is more nuanced than a simple “good” or “bad” label.

Take iPads, for instance. They’re versatile devices that can enrich life in many ways: you can read books, watch educational content from The Money Guy Show, create art, write articles, or follow fitness apps and videos. Yet, they can also be detrimental—maybe you spend 8 hours a day watching mindless TV on it, or develop a sports betting habit through apps available on the device.

Credit cards, like any tool, can be helpful or harmful depending on how you use them. Here’s how to use them properly to make them a valuable part of your financial toolkit—and what mistakes to steer clear of.

Advantages of using credit cards

Credit cards are often the most convenient payment method. Transactions are quick: a simple tap or inserting the card’s chip into a reader is all it takes. Gone are the days of counting coins or writing paper checks. But this convenience comes with a caveat—and a risk: you don’t even need to have the money in your bank account to complete a transaction.

Merchants face higher costs to accept credit cards due to processing fees. While some business owners charge extra to credit card users, most keep prices the same for both credit card users and those paying with cash or cash equivalents (like debit cards). This means if you pay with cash or non-reward debit cards, you’re effectively subsidizing credit card fees. The Federal Reserve estimates that each U.S. household using credit cards gets an annual “wealth transfer” of $1,133 from cash users.

Beyond convenience and this indirect cost advantage, credit cards offer other common benefits:

- Fraud protection: When shopping, credit cards add an extra layer of security. By law, your liability for unauthorized transactions is capped at $50, and most issuers offer zero-fraud-liability policies.

- Points or rewards: Many cards offer cash back (redeemable as statement credits or similar), while others provide rewards for specific uses—like travel miles or gift card points.

- Extended warranties: This is one of the most valuable features. For big purchases (such as expensive appliances or TVs), using a card with extended warranty coverage can help replace the item if it malfunctions later.

- Price matching: Some cards offer price matching—if you buy something and the price drops later, you can get a credit for the difference.

- Insurance: Travel or trip insurance is common—covering flight delays or lost luggage, which is great for frequent travelers.

Credit card mistakes to avoid

Why might someone avoid credit cards, then? They’re convenient, let you effectively pay less via rewards, and come with perks like price matching or insurance. But these benefits have a cost—and credit card companies aren’t acting out of kindness.

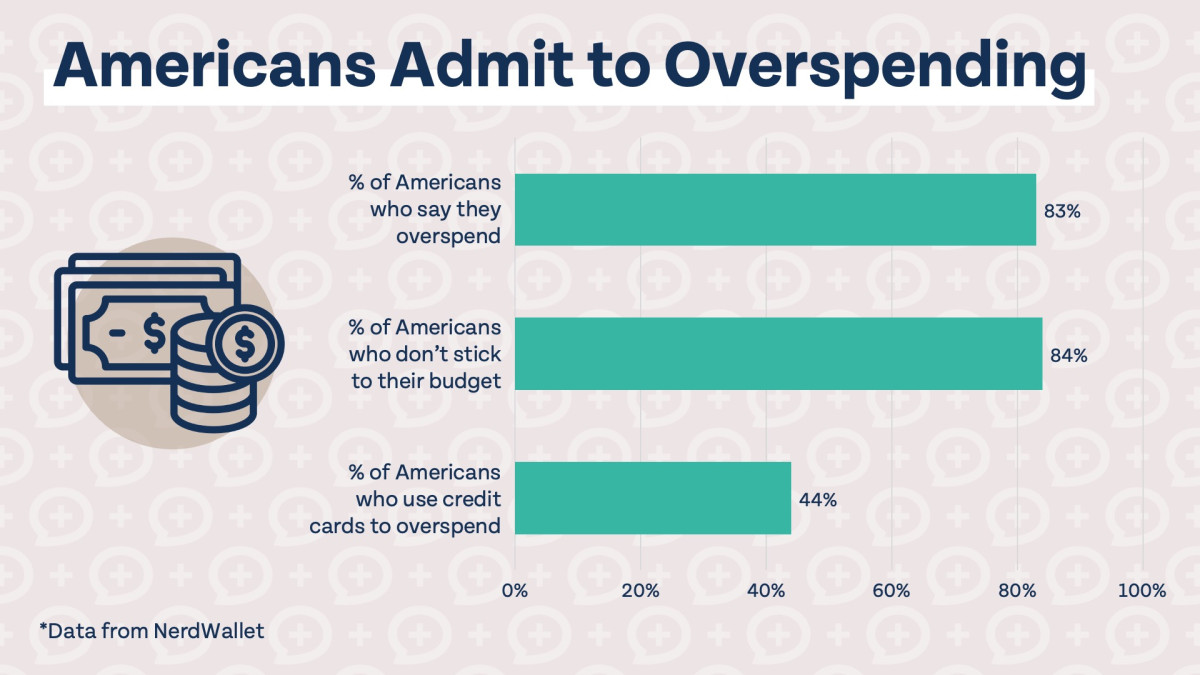

The biggest risk is overspending. Studies show people spend 12% to 18% more, on average, when using credit cards. Credit card transactions often feel less “real” than seeing cash leave your hand or money deducted from your bank account. Even if you pay your balance in full monthly, you might still spend more than you would without a credit card. Rewards and benefits can offset some of this extra spending, but not all. Given that most Americans spend 12% to 18% more with credit cards, it’s reasonable to say many might be better off not using them at all.

Unless you have extra income to cover overspending on credit cards, it will inevitably lead to credit card debt. Just typing that feels unsettling—almost like a dentist warning that skipping brushing leads to cavities, tooth decay, and eventually root canals. And credit card debt might even be more unpleasant than a trip to the dentist.

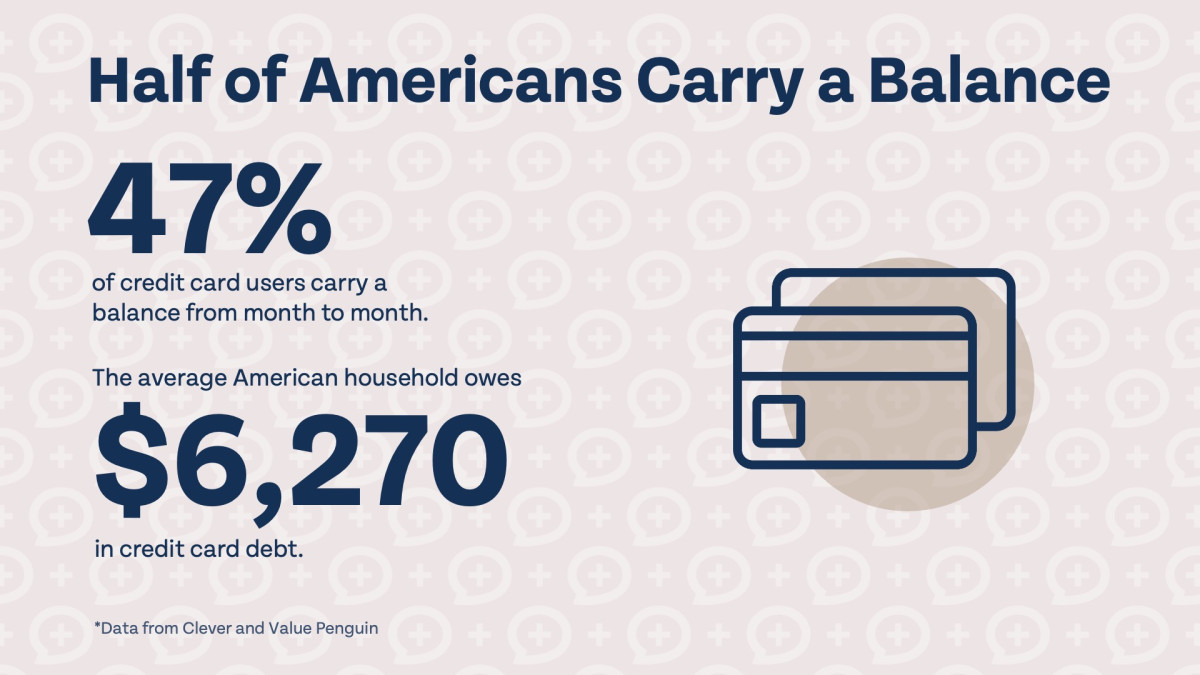

Credit card debt is particularly damaging because it turns compound interest into a weapon against you. Not only does it use compounding to your detriment, but the average credit card interest rate—24.20%—is far higher than the returns you’d typically get from investing in the stock market. Unfortunately, nearly half of all credit card users carry a balance from one month to the next.

When used correctly, credit cards can offer financial perks—but they can wreak havoc on your finances if you carry a balance. If you struggle to rein in your spending when using credit cards, there’s no shame in skipping their benefits and sticking solely to debit cards. And if you’re prone to overspending and end up carrying a credit card balance, the advantages of using credit cards become negligible next to the damage that credit card debt can do.

Home

detail

Why Credit Cards May Prove a Hazardous Weapon—or a Potent Tool

2025-08-26T17:34:34

Some financial influencers argue that credit cards should never be used, while others view them as a useful tool in managing personal finances. Are credit cards harmful, or are they beneficial? The reality is more nuanced than a simple “good” or “bad” label.

Take iPads, for instance. They’re versatile devices that can enrich life in many ways: you can read books, watch educational content from The Money Guy Show, create art, write articles, or follow fitness apps and videos. Yet, they can also be detrimental—maybe you spend 8 hours a day watching mindless TV on it, or develop a sports betting habit through apps available on the device.

Credit cards, like any tool, can be helpful or harmful depending on how you use them. Here’s how to use them properly to make them a valuable part of your financial toolkit—and what mistakes to steer clear of.

Advantages of using credit cards

Credit cards are often the most convenient payment method. Transactions are quick: a simple tap or inserting the card’s chip into a reader is all it takes. Gone are the days of counting coins or writing paper checks. But this convenience comes with a caveat—and a risk: you don’t even need to have the money in your bank account to complete a transaction.

Merchants face higher costs to accept credit cards due to processing fees. While some business owners charge extra to credit card users, most keep prices the same for both credit card users and those paying with cash or cash equivalents (like debit cards). This means if you pay with cash or non-reward debit cards, you’re effectively subsidizing credit card fees. The Federal Reserve estimates that each U.S. household using credit cards gets an annual “wealth transfer” of $1,133 from cash users.

Beyond convenience and this indirect cost advantage, credit cards offer other common benefits:

- Fraud protection: When shopping, credit cards add an extra layer of security. By law, your liability for unauthorized transactions is capped at $50, and most issuers offer zero-fraud-liability policies.

- Points or rewards: Many cards offer cash back (redeemable as statement credits or similar), while others provide rewards for specific uses—like travel miles or gift card points.

- Extended warranties: This is one of the most valuable features. For big purchases (such as expensive appliances or TVs), using a card with extended warranty coverage can help replace the item if it malfunctions later.

- Price matching: Some cards offer price matching—if you buy something and the price drops later, you can get a credit for the difference.

- Insurance: Travel or trip insurance is common—covering flight delays or lost luggage, which is great for frequent travelers.

Credit card mistakes to avoid

Why might someone avoid credit cards, then? They’re convenient, let you effectively pay less via rewards, and come with perks like price matching or insurance. But these benefits have a cost—and credit card companies aren’t acting out of kindness.

The biggest risk is overspending. Studies show people spend 12% to 18% more, on average, when using credit cards. Credit card transactions often feel less “real” than seeing cash leave your hand or money deducted from your bank account. Even if you pay your balance in full monthly, you might still spend more than you would without a credit card. Rewards and benefits can offset some of this extra spending, but not all. Given that most Americans spend 12% to 18% more with credit cards, it’s reasonable to say many might be better off not using them at all.

Unless you have extra income to cover overspending on credit cards, it will inevitably lead to credit card debt. Just typing that feels unsettling—almost like a dentist warning that skipping brushing leads to cavities, tooth decay, and eventually root canals. And credit card debt might even be more unpleasant than a trip to the dentist.

Credit card debt is particularly damaging because it turns compound interest into a weapon against you. Not only does it use compounding to your detriment, but the average credit card interest rate—24.20%—is far higher than the returns you’d typically get from investing in the stock market. Unfortunately, nearly half of all credit card users carry a balance from one month to the next.

When used correctly, credit cards can offer financial perks—but they can wreak havoc on your finances if you carry a balance. If you struggle to rein in your spending when using credit cards, there’s no shame in skipping their benefits and sticking solely to debit cards. And if you’re prone to overspending and end up carrying a credit card balance, the advantages of using credit cards become negligible next to the damage that credit card debt can do.