Money is a fundamental necessity, much like food, water, and housing. In fact, it might even be a more critical need—after all, you can rarely eat, drink, or have a safe place to stay without it. Each of us has a unique relationship with money, shaped by our experiences as children and working adults. For some, money is a scarce and valuable resource; for others, it’s abundant, spent without much thought.

I think one of the main reasons for cyclical poverty (or even living paycheck to paycheck) is an unhealthy relationship with money—often caused, at least in part, by impactful, formative experiences in childhood. The reverse also holds true: a healthy relationship with money is a key factor in building generational wealth. There are other contributing elements, some possibly more significant, but in this article, I want to focus on how to build a healthy money relationship and how it might help you break the paycheck-to-paycheck cycle.

Compare yourself to others as little as possible

Financially, comparing yourself to others is a losing game. There will always be someone with more money, a nicer house, car, or clothes. Growing up, my family wasn’t poor, but we were far from wealthy. As a kid, I wanted brand-name clothes to show we were “doing as well as” others. I felt ashamed when other kids got the latest game console for Christmas and we didn’t. I wondered why we used so many grocery coupons while other families didn’t.

It wasn’t until I had a full-time job as an adult that I started to feel proud of my parents’ financial habits. We didn’t always get the newest clothes or games, but we always had food, clean clothes, and a warm bed. Until I was around 25, I’d spent my life longing to have as much as everyone else—but I realized that didn’t matter as much as I once thought. Who cares if my clothes are name-brand if I like what I’m wearing? So what if we use coupons? Many wealthy people actually love being frugal and saving.

Resisting the urge to compare financially is easier said than done, but comparison can stop you from appreciating what you have. It keeps you on a never-ending financial hamster wheel, chasing a top you’ll never reach.

Teach yourself about money

My parents had no idea what a Roth IRA was or how powerful an HSA could be. They taught me saving money (in a savings account) was important, but not much else. Formal financial education didn’t come my way until college. When I started learning more about personal finance, my perspective shifted entirely. I realized regular people could build wealth—I’d always thought investing was just for the rich.

Many Americans lack financial literacy, and you might be one of them—and that’s okay! It’s never been easier to educate yourself about money and learn to build wealth. The Money Guy Show is a great resource. Whether you’re trying to get out of debt, stop living paycheck to paycheck, or explore advanced investing strategies beyond the usual Roth IRA or 401(k), they have content to help. Their “Financial Order of Operations” is an excellent starting point if you’re not sure what to do next.

When educating yourself about personal finance, be proactive, not complacent. Keep an open mind—what you learned when you were young might not be true.

Use budgeting tools to stay on track

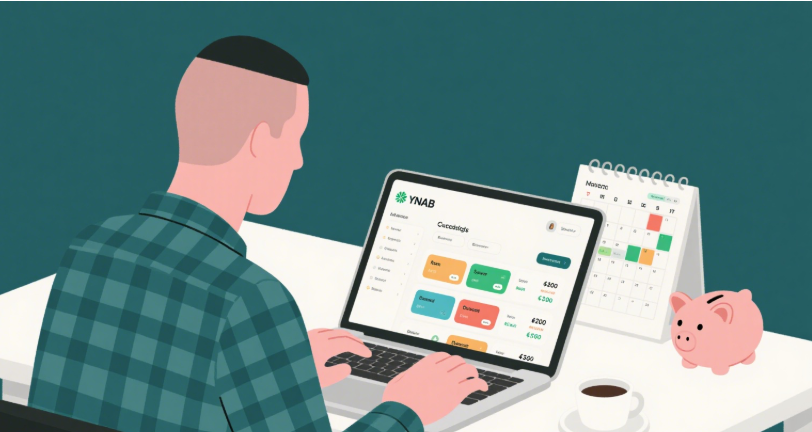

For me, budgeting was key to building a healthy money relationship. Without a budget, I spent every dollar I made each month. If I had money left at the end of the month, I’d find something to spend it on. Budgeting helped me see how wasteful some of my spending was. It let me set financial goals and set aside money for future saving and spending. I used (and still use) the popular app YNAB, which is built around “giving every dollar a job” as soon as you earn it.

This method worked really well. Every dollar had a purpose right away—no more money sitting in my bank account, waiting to be spent impulsively. I even started budgeting months in advance: the money I earned in January would be assigned to categories for May. Rent, Roth IRA contributions, dining out, groceries, electric bills—all covered well ahead of time. I felt like I had little extra spending money because every dollar was earmarked, but in reality, I had plenty of potential spending cash—it just “didn’t exist” to me because it was already assigned.

Once budgeting and spending become second nature, you might move to a cash management plan, where you can save what you need each month without a strict budget. Personally, I still use a budget and don’t plan to stop. I know I naturally spend less and save more when I plan where every dollar goes in advance.

Allow yourself a reasonable amount of spending

When I started budgeting, I quickly learned I’d burn out if I didn’t set aside money for spontaneous, lighthearted spending. A big part of a healthy money relationship is being able to spend what you can afford without guilt or shame. People at all income and wealth levels struggle with this.

One reason I’ve noticed people avoid “unnecessary” spending is uncertainty about their financial habits. They don’t know if they’re saving enough for the future, so they over-restrict spending to save more, just to be safe. Finding balance is hard—you can easily go from underspending (crazy as that sounds) to overspending.

The key to balance is identifying your financial goals, figuring out what you need to do to reach them, and making a plan that accounts for as many “unknowns” as possible (like investment returns, income changes, major life events, or inflation). Our “Know Your Number” course is a good place to start thinking about these goals and what they’ll take. For those who want a second opinion or a financial “co-pilot,” meeting with a fee-only financial advisor is a great next step.

A healthy relationship with money doesn’t develop overnight. If you think yours is unhealthy now, you can overcome old habits and beliefs—but it takes time. As someone who’s seen their own relationship with money shift dramatically (and grow healthier) over the years, I can say for sure: starting today is worth it. It can leave you happier, more secure, and confident in your finances.

Home

detail

Ways to Cultivate a Positive Relationship With Money

2025-08-26T17:30:43

Money is a fundamental necessity, much like food, water, and housing. In fact, it might even be a more critical need—after all, you can rarely eat, drink, or have a safe place to stay without it. Each of us has a unique relationship with money, shaped by our experiences as children and working adults. For some, money is a scarce and valuable resource; for others, it’s abundant, spent without much thought.

I think one of the main reasons for cyclical poverty (or even living paycheck to paycheck) is an unhealthy relationship with money—often caused, at least in part, by impactful, formative experiences in childhood. The reverse also holds true: a healthy relationship with money is a key factor in building generational wealth. There are other contributing elements, some possibly more significant, but in this article, I want to focus on how to build a healthy money relationship and how it might help you break the paycheck-to-paycheck cycle.

Compare yourself to others as little as possible

Financially, comparing yourself to others is a losing game. There will always be someone with more money, a nicer house, car, or clothes. Growing up, my family wasn’t poor, but we were far from wealthy. As a kid, I wanted brand-name clothes to show we were “doing as well as” others. I felt ashamed when other kids got the latest game console for Christmas and we didn’t. I wondered why we used so many grocery coupons while other families didn’t.

It wasn’t until I had a full-time job as an adult that I started to feel proud of my parents’ financial habits. We didn’t always get the newest clothes or games, but we always had food, clean clothes, and a warm bed. Until I was around 25, I’d spent my life longing to have as much as everyone else—but I realized that didn’t matter as much as I once thought. Who cares if my clothes are name-brand if I like what I’m wearing? So what if we use coupons? Many wealthy people actually love being frugal and saving.

Resisting the urge to compare financially is easier said than done, but comparison can stop you from appreciating what you have. It keeps you on a never-ending financial hamster wheel, chasing a top you’ll never reach.

Teach yourself about money

My parents had no idea what a Roth IRA was or how powerful an HSA could be. They taught me saving money (in a savings account) was important, but not much else. Formal financial education didn’t come my way until college. When I started learning more about personal finance, my perspective shifted entirely. I realized regular people could build wealth—I’d always thought investing was just for the rich.

Many Americans lack financial literacy, and you might be one of them—and that’s okay! It’s never been easier to educate yourself about money and learn to build wealth. The Money Guy Show is a great resource. Whether you’re trying to get out of debt, stop living paycheck to paycheck, or explore advanced investing strategies beyond the usual Roth IRA or 401(k), they have content to help. Their “Financial Order of Operations” is an excellent starting point if you’re not sure what to do next.

When educating yourself about personal finance, be proactive, not complacent. Keep an open mind—what you learned when you were young might not be true.

Use budgeting tools to stay on track

For me, budgeting was key to building a healthy money relationship. Without a budget, I spent every dollar I made each month. If I had money left at the end of the month, I’d find something to spend it on. Budgeting helped me see how wasteful some of my spending was. It let me set financial goals and set aside money for future saving and spending. I used (and still use) the popular app YNAB, which is built around “giving every dollar a job” as soon as you earn it.

This method worked really well. Every dollar had a purpose right away—no more money sitting in my bank account, waiting to be spent impulsively. I even started budgeting months in advance: the money I earned in January would be assigned to categories for May. Rent, Roth IRA contributions, dining out, groceries, electric bills—all covered well ahead of time. I felt like I had little extra spending money because every dollar was earmarked, but in reality, I had plenty of potential spending cash—it just “didn’t exist” to me because it was already assigned.

Once budgeting and spending become second nature, you might move to a cash management plan, where you can save what you need each month without a strict budget. Personally, I still use a budget and don’t plan to stop. I know I naturally spend less and save more when I plan where every dollar goes in advance.

Allow yourself a reasonable amount of spending

When I started budgeting, I quickly learned I’d burn out if I didn’t set aside money for spontaneous, lighthearted spending. A big part of a healthy money relationship is being able to spend what you can afford without guilt or shame. People at all income and wealth levels struggle with this.

One reason I’ve noticed people avoid “unnecessary” spending is uncertainty about their financial habits. They don’t know if they’re saving enough for the future, so they over-restrict spending to save more, just to be safe. Finding balance is hard—you can easily go from underspending (crazy as that sounds) to overspending.

The key to balance is identifying your financial goals, figuring out what you need to do to reach them, and making a plan that accounts for as many “unknowns” as possible (like investment returns, income changes, major life events, or inflation). Our “Know Your Number” course is a good place to start thinking about these goals and what they’ll take. For those who want a second opinion or a financial “co-pilot,” meeting with a fee-only financial advisor is a great next step.

A healthy relationship with money doesn’t develop overnight. If you think yours is unhealthy now, you can overcome old habits and beliefs—but it takes time. As someone who’s seen their own relationship with money shift dramatically (and grow healthier) over the years, I can say for sure: starting today is worth it. It can leave you happier, more secure, and confident in your finances.