Need immediate help? Our nonprofit financial counselors can review your medical bills and outline personalized relief options—at no cost to you.

In this guide, we’ll cover:

- Quick actions to take today (no waiting required)

- Step-by-step process to lower or organize medical bills

- Angela’s story (a 2-minute read of how one family found relief)

- FAQs about medical debt solutions

- How to get help from a nonprofit counselor

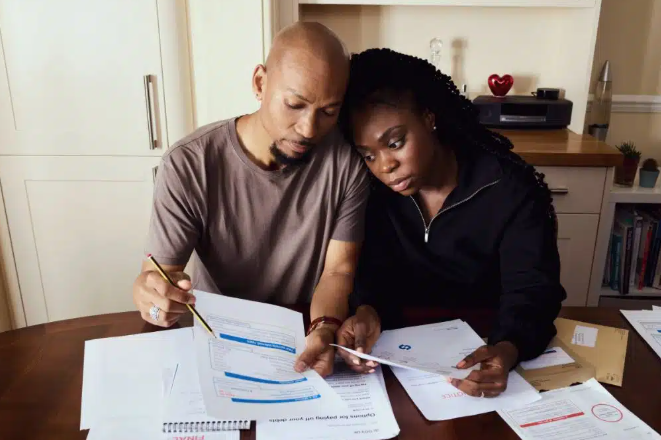

Medical bills aren’t like regular monthly expenses—they often come from multiple providers, with confusing statements, and timing gaps with insurance claims. Even small unpaid balances can snowball, especially when paired with credit card debt or collections. This guide breaks down clear, actionable steps to manage your bills, plus how this site nonprofit counseling can help you build a plan that fits your budget.

Quick Actions to Take Today

Don’t let medical debt feel overwhelming—start with these simple, impactful steps:

- Request an itemized bill from every provider, then compare it to your Explanation of Benefits (EOB). If you spot errors (e.g., duplicate charges, services you didn’t receive), dispute them in writing.

- Ask providers for a 0% interest payment plan with a monthly amount you can reliably afford—and get all terms in writing (no verbal agreements!).

- Check for hospital financial assistance (charity care) if you received care at a nonprofit facility. Ask about eligibility rules and what documents you’ll need to apply.

- Prioritize essential expenses first: Cover housing, utilities, food, and transportation before putting money toward medical collections.

Step-by-Step: How to Lower or Organize Your Medical Bills

Follow this structured process to take control of your medical debt—no prior financial experience needed.

1. Review Your Bill and Fix Errors

First, ask each provider for a detailed, itemized bill (not just a summary). Check every line item:

- Confirm dates match your appointments.

- Verify medical codes (e.g., a routine checkup shouldn’t be coded as an emergency visit).

- Ensure quantities or services align with what you received (e.g., you weren’t charged for 10 pills if you only got 5).

Compare the itemized bill to your EOB (the document from your insurance company). If something doesn’t add up, send a written dispute to both the provider’s billing department and your insurer. Attach proof (like your EOB, appointment notes, or receipts) and keep copies of all correspondence for your records.

2. Negotiate a Realistic Payment Plan

Most medical providers are willing to set up 0% interest payment plans—you just need to ask. When discussing terms:

- Propose a monthly payment that fits your budget (even small, consistent payments are better than missing large ones).

- Get all details in writing: payment amount, due date, length of the plan, and whether late fees apply.

- Avoid agreeing to a plan you can’t sustain—missing payments could lead to collections or penalty fees.

3. Apply for Hospital Financial Assistance (Charity Care)

Nonprofit hospitals are required to publish Financial Assistance Policies (FAPs), which outline:

- Income limits for eligibility (e.g., households earning below 200% of the federal poverty line may qualify for reduced or free care).

- Required documents (e.g., pay stubs, tax returns, proof of household size).

- Timeframes for applying (some hospitals require applications within 6 months of service).

If approved, your bill could be significantly reduced—or even written off entirely. Ask the hospital’s billing office how to apply and whether the assistance covers already-issued bills.

4. Consolidate Debts with a Debt Management Plan (DMP) (If Needed)

If medical bills are piling up alongside credit cards or other unsecured debts, a Debt Management Plan (DMP) can simplify your finances. Here’s how it works:

- You make one structured monthly payment to a nonprofit credit counseling agency .

- The agency distributes funds to your creditors (including participating medical providers).

- Many creditors reduce or waive interest rates and late fees for DMP participants.

Important notes:

- A DMP is not a loan—there’s no new debt involved.

- There’s no hard credit pull to start counseling (your credit score won’t be hurt by the initial review).

- Eligibility and benefits vary by creditor and your financial situation—your counselor will confirm details before you enroll.

5. Handle Medical Bills in Collections

If your medical debt is already in collections:

- Ask the collector for a detailed account history (they’re required by law to provide this if you request it).

- Propose a payment plan you can afford—and get the agreement in writing (never pay a collector without a written record).

- Avoid opening high-cost credit (like payday loans or high-APR credit cards) to cover the debt—this will only make your financial situation worse.

6. Avoid Common Medical Debt Pitfalls

Steer clear of these mistakes that can prolong your debt:

- Medical credit cards or high-APR financing: Promotional 0% rates often expire, leaving you with sky-high interest (sometimes 20%+).

- Overpromising on payments: Agreeing to a $300/month plan when you can only afford $100 will lead to missed payments and more stress.

- Ignoring bills: Unpaid medical bills can go to collections, hurt your credit score, and even lead to lawsuits (in some cases).

7. Gather the Right Documents Before Getting Help

When working with a counselor or negotiating with providers, have these ready:

- All itemized medical bills and EOBs.

- Account numbers, due dates, and contact info for each provider.

- Your monthly take-home income (pay stubs, side hustle earnings, etc.).

- A list of essential monthly expenses (housing, utilities, food, transportation).

Angela’s Story: How She Got Out of Medical Debt

Angela, a working parent, felt crushed under a pile of medical bills: hospital stays, lab tests, imaging, and specialist visits—plus rising credit card debt from covering co-pays. Her provider offered a short-term payment plan with $400 monthly payments, which she couldn’t afford on her salary. Notices kept arriving in the mail, and she worried about missing payments and hurting her credit.

She reached out for nonprofit counseling. Her counselor:

- Reviewed all her itemized bills and EOBs to check for errors.

- Confirmed the provider’s payment plan wasn’t feasible for her budget.

- Helped her enroll in a Debt Management Plan (DMP) that consolidated her medical bills and credit card debt into one $250 monthly payment—an amount she could easily cover.

With the DMP, Angela’s eligible debts were set on a payoff schedule projected to be under 5 years. For the first time in months, she didn’t have to juggle multiple due dates or stress about collections. “I can focus on my family now, not my bills,” she said.

Every situation is unique—creditor participation, terms, and outcomes vary based on individual circumstances.

FAQs About Medical Debt Relief

Can medical bills be included in a Debt Management Plan (DMP)?

Sometimes—if the medical provider participates in DMP programs and the account is eligible (e.g., not in active litigation). Your counselor will review your bills and confirm which accounts can be included before you enroll.

Will a DMP or medical debt relief affect my credit score?

A DMP itself isn’t a loan, so there’s no hard credit inquiry to start counseling. Your credit score may change based on:

- Payment history (on-time payments through a DMP can help improve your score over time).

- Credit utilization (closing accounts to new charges—common with DMPs—may temporarily lower your score, but this often rebounds as you pay down debt).

Unpaid medical bills in collections, however, can hurt your credit score—so addressing them quickly is key.

Do hospitals have to offer financial assistance?

Nonprofit hospitals are required by law to have a Financial Assistance Policy (FAP) and make it available to patients. Eligibility (e.g., income limits) and benefits (e.g., reduced bills vs. free care) vary by hospital. For-profit hospitals may offer assistance programs voluntarily, but they aren’t required to.

Is bankruptcy ever a good option for medical debt?

Bankruptcy is a last resort, but it may be necessary if you have overwhelming medical debt that you can’t manage with other solutions (like payment plans or financial assistance). A nonprofit counselor can help you assess whether bankruptcy is right for you and refer you to trusted legal resources if needed.

Home

detail

Medical Debt Relief: How to Reduce, Organize Bills & Regain Financial Control

2025-09-09T14:05:50

Need immediate help? Our nonprofit financial counselors can review your medical bills and outline personalized relief options—at no cost to you.

In this guide, we’ll cover:

- Quick actions to take today (no waiting required)

- Step-by-step process to lower or organize medical bills

- Angela’s story (a 2-minute read of how one family found relief)

- FAQs about medical debt solutions

- How to get help from a nonprofit counselor

Medical bills aren’t like regular monthly expenses—they often come from multiple providers, with confusing statements, and timing gaps with insurance claims. Even small unpaid balances can snowball, especially when paired with credit card debt or collections. This guide breaks down clear, actionable steps to manage your bills, plus how this site nonprofit counseling can help you build a plan that fits your budget.

Quick Actions to Take Today

Don’t let medical debt feel overwhelming—start with these simple, impactful steps:

- Request an itemized bill from every provider, then compare it to your Explanation of Benefits (EOB). If you spot errors (e.g., duplicate charges, services you didn’t receive), dispute them in writing.

- Ask providers for a 0% interest payment plan with a monthly amount you can reliably afford—and get all terms in writing (no verbal agreements!).

- Check for hospital financial assistance (charity care) if you received care at a nonprofit facility. Ask about eligibility rules and what documents you’ll need to apply.

- Prioritize essential expenses first: Cover housing, utilities, food, and transportation before putting money toward medical collections.

Step-by-Step: How to Lower or Organize Your Medical Bills

Follow this structured process to take control of your medical debt—no prior financial experience needed.

1. Review Your Bill and Fix Errors

First, ask each provider for a detailed, itemized bill (not just a summary). Check every line item:

- Confirm dates match your appointments.

- Verify medical codes (e.g., a routine checkup shouldn’t be coded as an emergency visit).

- Ensure quantities or services align with what you received (e.g., you weren’t charged for 10 pills if you only got 5).

Compare the itemized bill to your EOB (the document from your insurance company). If something doesn’t add up, send a written dispute to both the provider’s billing department and your insurer. Attach proof (like your EOB, appointment notes, or receipts) and keep copies of all correspondence for your records.

2. Negotiate a Realistic Payment Plan

Most medical providers are willing to set up 0% interest payment plans—you just need to ask. When discussing terms:

- Propose a monthly payment that fits your budget (even small, consistent payments are better than missing large ones).

- Get all details in writing: payment amount, due date, length of the plan, and whether late fees apply.

- Avoid agreeing to a plan you can’t sustain—missing payments could lead to collections or penalty fees.

3. Apply for Hospital Financial Assistance (Charity Care)

Nonprofit hospitals are required to publish Financial Assistance Policies (FAPs), which outline:

- Income limits for eligibility (e.g., households earning below 200% of the federal poverty line may qualify for reduced or free care).

- Required documents (e.g., pay stubs, tax returns, proof of household size).

- Timeframes for applying (some hospitals require applications within 6 months of service).

If approved, your bill could be significantly reduced—or even written off entirely. Ask the hospital’s billing office how to apply and whether the assistance covers already-issued bills.

4. Consolidate Debts with a Debt Management Plan (DMP) (If Needed)

If medical bills are piling up alongside credit cards or other unsecured debts, a Debt Management Plan (DMP) can simplify your finances. Here’s how it works:

- You make one structured monthly payment to a nonprofit credit counseling agency .

- The agency distributes funds to your creditors (including participating medical providers).

- Many creditors reduce or waive interest rates and late fees for DMP participants.

Important notes:

- A DMP is not a loan—there’s no new debt involved.

- There’s no hard credit pull to start counseling (your credit score won’t be hurt by the initial review).

- Eligibility and benefits vary by creditor and your financial situation—your counselor will confirm details before you enroll.

5. Handle Medical Bills in Collections

If your medical debt is already in collections:

- Ask the collector for a detailed account history (they’re required by law to provide this if you request it).

- Propose a payment plan you can afford—and get the agreement in writing (never pay a collector without a written record).

- Avoid opening high-cost credit (like payday loans or high-APR credit cards) to cover the debt—this will only make your financial situation worse.

6. Avoid Common Medical Debt Pitfalls

Steer clear of these mistakes that can prolong your debt:

- Medical credit cards or high-APR financing: Promotional 0% rates often expire, leaving you with sky-high interest (sometimes 20%+).

- Overpromising on payments: Agreeing to a $300/month plan when you can only afford $100 will lead to missed payments and more stress.

- Ignoring bills: Unpaid medical bills can go to collections, hurt your credit score, and even lead to lawsuits (in some cases).

7. Gather the Right Documents Before Getting Help

When working with a counselor or negotiating with providers, have these ready:

- All itemized medical bills and EOBs.

- Account numbers, due dates, and contact info for each provider.

- Your monthly take-home income (pay stubs, side hustle earnings, etc.).

- A list of essential monthly expenses (housing, utilities, food, transportation).

Angela’s Story: How She Got Out of Medical Debt

Angela, a working parent, felt crushed under a pile of medical bills: hospital stays, lab tests, imaging, and specialist visits—plus rising credit card debt from covering co-pays. Her provider offered a short-term payment plan with $400 monthly payments, which she couldn’t afford on her salary. Notices kept arriving in the mail, and she worried about missing payments and hurting her credit.

She reached out for nonprofit counseling. Her counselor:

- Reviewed all her itemized bills and EOBs to check for errors.

- Confirmed the provider’s payment plan wasn’t feasible for her budget.

- Helped her enroll in a Debt Management Plan (DMP) that consolidated her medical bills and credit card debt into one $250 monthly payment—an amount she could easily cover.

With the DMP, Angela’s eligible debts were set on a payoff schedule projected to be under 5 years. For the first time in months, she didn’t have to juggle multiple due dates or stress about collections. “I can focus on my family now, not my bills,” she said.

Every situation is unique—creditor participation, terms, and outcomes vary based on individual circumstances.

FAQs About Medical Debt Relief

Can medical bills be included in a Debt Management Plan (DMP)?

Sometimes—if the medical provider participates in DMP programs and the account is eligible (e.g., not in active litigation). Your counselor will review your bills and confirm which accounts can be included before you enroll.

Will a DMP or medical debt relief affect my credit score?

A DMP itself isn’t a loan, so there’s no hard credit inquiry to start counseling. Your credit score may change based on:

- Payment history (on-time payments through a DMP can help improve your score over time).

- Credit utilization (closing accounts to new charges—common with DMPs—may temporarily lower your score, but this often rebounds as you pay down debt).

Unpaid medical bills in collections, however, can hurt your credit score—so addressing them quickly is key.

Do hospitals have to offer financial assistance?

Nonprofit hospitals are required by law to have a Financial Assistance Policy (FAP) and make it available to patients. Eligibility (e.g., income limits) and benefits (e.g., reduced bills vs. free care) vary by hospital. For-profit hospitals may offer assistance programs voluntarily, but they aren’t required to.

Is bankruptcy ever a good option for medical debt?

Bankruptcy is a last resort, but it may be necessary if you have overwhelming medical debt that you can’t manage with other solutions (like payment plans or financial assistance). A nonprofit counselor can help you assess whether bankruptcy is right for you and refer you to trusted legal resources if needed.